Copper Is Quietly Becoming the Most Important Metal in the System

First off, thank you again to everyone reading Fiat’s Funeral and sticking with me through gold and silver’s recent rollercoaster.

Today, I want to zoom out and talk about the metal that quietly sits behind almost every “future of the economy” buzzword you’ve heard in the last five years:

Copper.

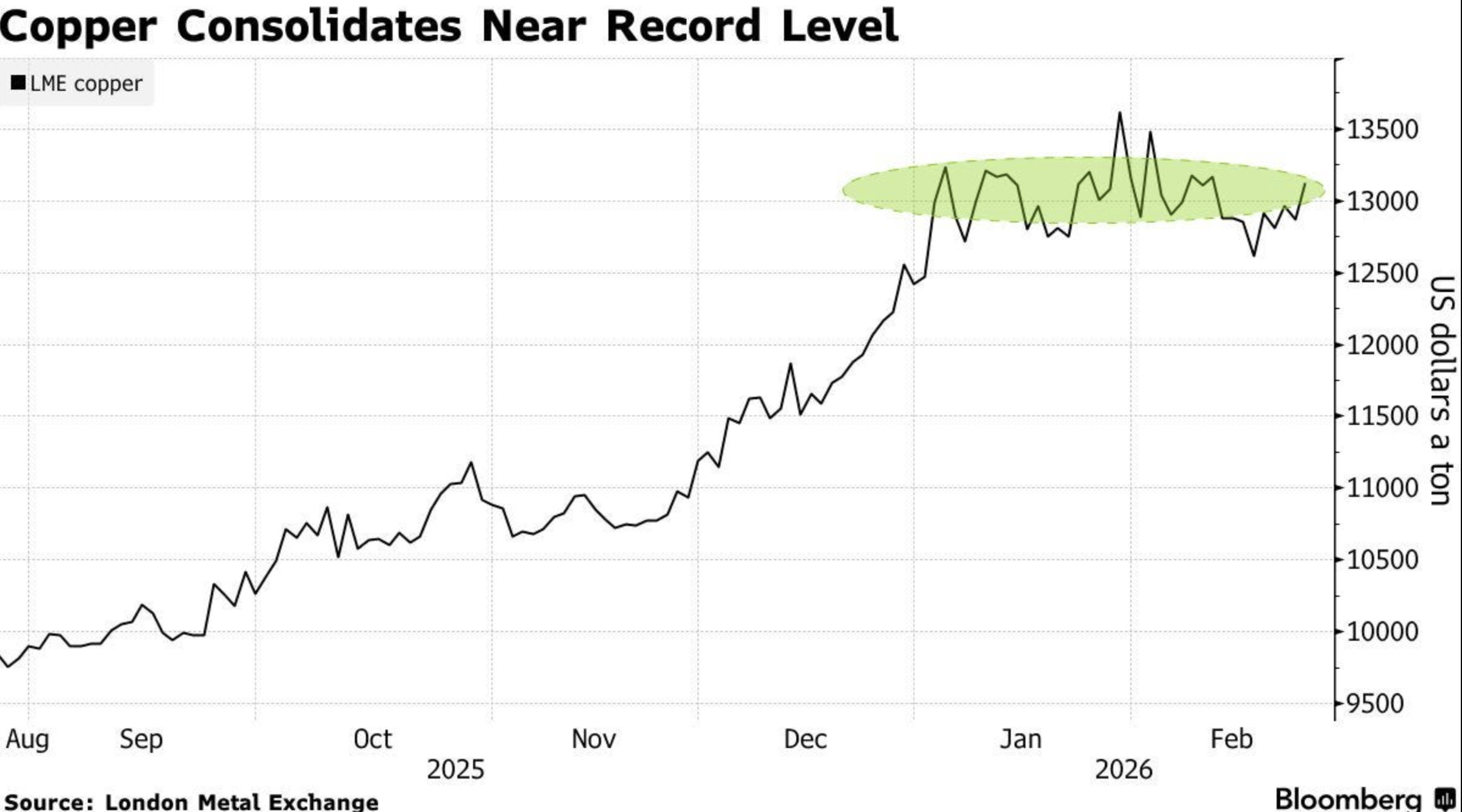

While the world was arguing over whether gold and silver had “turned into memes,” copper quietly broke to record highs, then pulled back just enough to make people doubt themselves again. I think that’s a mistake.

This isn’t a trade I’m chasing for tomorrow’s candle. It’s a structural story that could easily make copper one of the next big runners in the commodities complex.

1. Where copper sits today

Let’s start with the simple part: price.

Copper is trading around the $6 range per pound, after touching record levels above $6.5 earlier this year.

Even after the recent dip, it’s still more than 30% higher than it was a year ago and well above its 200‑day moving average.

Short‑term, the market’s cooled off a bit: over the last month the price has drifted slightly lower, which feels more like consolidation than a collapse.

In other words: we’re not at the bottom of a range. We’re living in a new range, and the market is trying to decide whether it overshot or not.

The interesting part is what the people who live and breathe this metal are saying.

2. What the serious money is forecasting

J.P. Morgan’s commodity team doesn’t exactly write meme threads, but their copper outlook reads like a quiet bull manifesto.

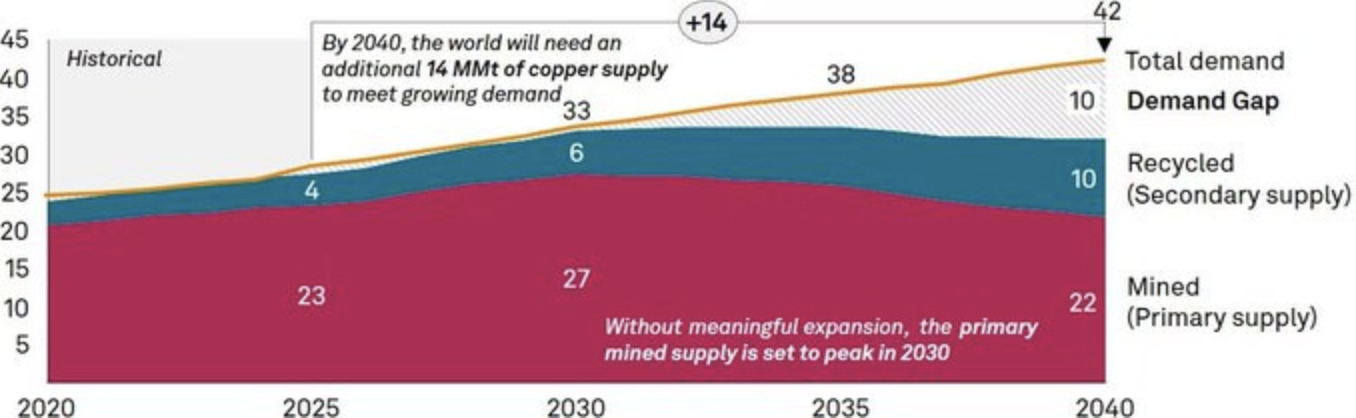

They’re projecting a global refined copper deficit of around 330,000 tonnes in 2026, driven by mine disruptions and demand that refuses to slow down.

On price, they expect copper to average roughly 12,075 dollars per ton in 2026, with a spike to around 12,500 dollars per ton in Q2 as the market tightens.

Citi goes a step further:

They see copper potentially pushing through 13,000 dollars per ton and approaching 15,000 if supply issues and low inventories collide with strong demand.

Even more cautious houses are still talking about “elevated” levels:

StoneX sees copper averaging close to 11,500 dollars per ton in 2026, while Bank of America and TD Cowen have nudged their 2026 forecasts up into the 5‑plus dollars per pound zone.

The tone isn’t “bubble about to pop.” It’s more like: “We didn’t think it would get here this fast, but the fundamental squeeze is real.”

3. Why the tape is tight: the three‑headed demand monster

Copper isn’t gold. Nobody buys it to stare at in a vault.

You need it to build the world we keep pretending we want:

Electrification and grids

Every serious decarbonization plan, from EVs to heat pumps to transmission lines for renewables, runs through copper.

AI data centers being the latest obsession are power hogs. More power means more transformers, more cables, more copper.

EVs and transport

Electric vehicles use significantly more copper than internal‑combustion cars, thanks to motors, wiring and charging infrastructure.

As EV penetration rises, copper gets pulled into both the vehicles and the networks that support them.

Emerging‑market build‑out

Countries that aren’t yet saturated with infrastructure still need traditional things: housing, rail, grids, factories.

Even if the West slows down, emerging‑market demand can keep the copper pipeline busy.

On the other side of the ledger, supply is not racing to keep up:

J.P. Morgan flags large, unexpected supply disruptions and delays at major mines as a key driver of the coming deficit.

The International Copper Study Group’s data show that a previous surplus shrank dramatically in 2025 as demand picked up and supply under‑delivered, setting the stage for today’s tightness.

Analysts at DWS describe a market “between shortage and stockpiling,” with low visible inventories helping keep prices near record highs.

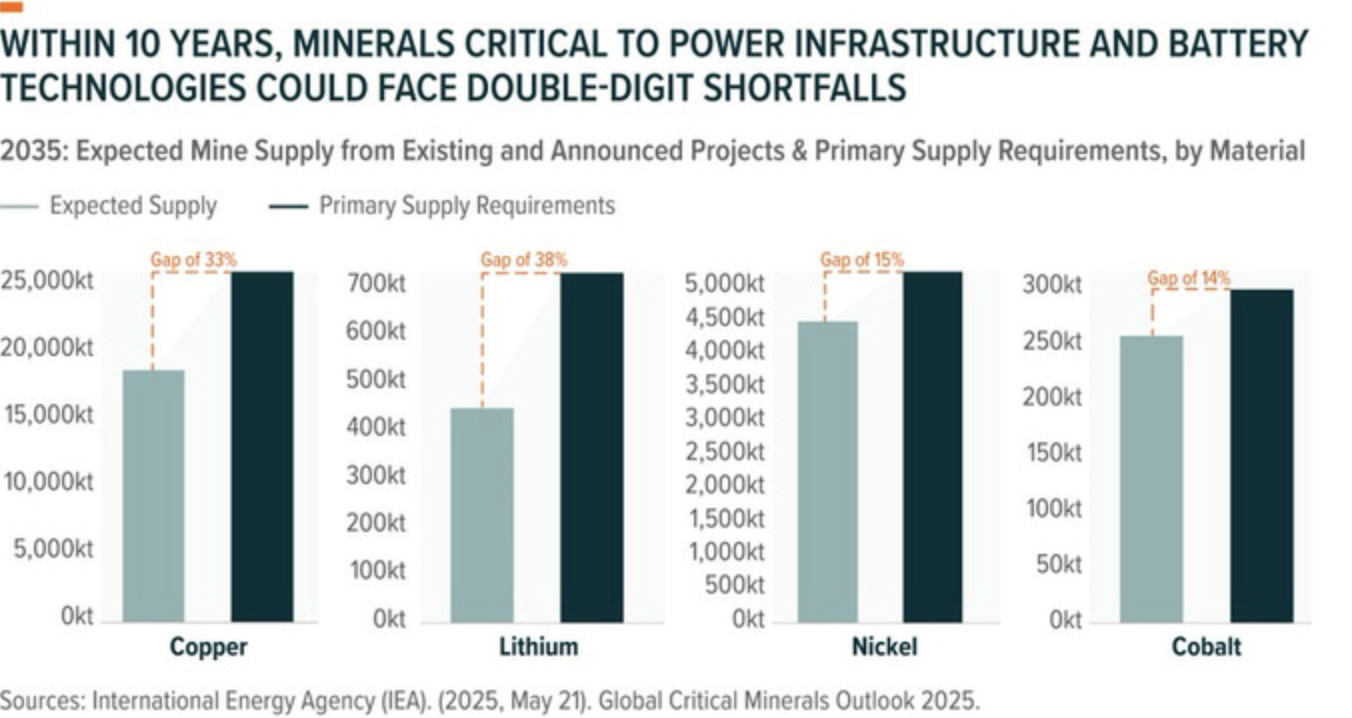

You don’t need to believe in the most extreme forecasts to see the shape of the story: structurally rising demand, chronic execution issues on the supply side, and very little slack in the system.

4. The problem nobody can engineer away

This is the part of the copper story that never shows up in price targets.

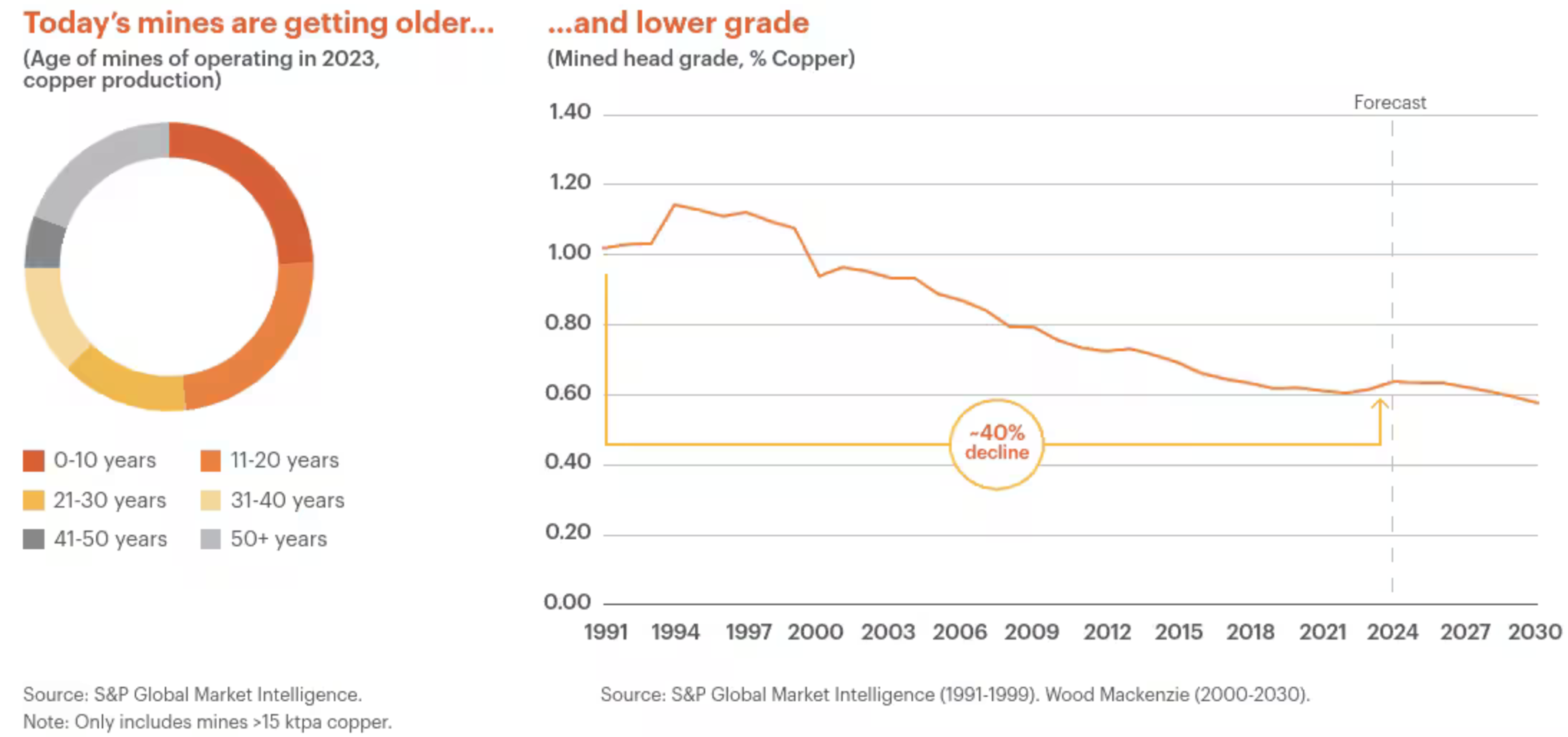

The world is running copper production off an aging asset base.

Most operating copper mines today were discovered decades ago, built decades ago, and are now being pushed harder just to maintain output. At the same time, the quality of what comes out of the ground keeps getting worse.

Average copper head grades have fallen roughly forty percent over the past three decades. That means miners must move, crush, and process far more rock just to produce the same pound of copper they did in the 1990s.

Older mines

Lower grades

Higher costs

More energy

More water

More permitting friction

That combination is toxic for supply growth.

You can throw capital at the problem, but geology does not care. You cannot financial engineer grade back into an orebody. You cannot optimize your way out of depletion.

This is why copper deficits keep showing up in forecasts even after years of higher prices. New supply takes longer, costs more, faces more political resistance, and still tends to come online at lower grades than the mines it replaces.

When people argue copper is overextended, this is the chart they are ignoring.

Higher prices are not the cause of the problem. They are the consequence of trying to stretch an aging, declining system to meet rising demand.

And once you see this, it becomes much harder to believe copper can simply drift back to “old normal” prices without breaking something on the supply side.

5. “Overextended” or early in a super‑cycle?

Not everyone is comfortable with where copper trades today.

Some analysts argue that this period of elevated prices has been “overextended,” pointing out that Chinese futures traders have built sizeable short positions and that sentiment may have run ahead of reality in the West. Goldman Sachs, for example, expects some cooling back toward the 10,000–11,000 dollar per ton range in 2026, even as they stay bullish longer term.

I actually like that split.

When you have:

Western institutions talking about shortages and secular demand,

Chinese traders leaning net short,

and big banks split between “too high” and “still going higher,”

…you get the exact mix of disagreement that can fuel big moves in both directions.

The largest and most experienced players in the mining world have been positioning for copper for years, not weeks. BHP has been openly framing copper as a cornerstone of its long term growth strategy, prioritizing organic expansion and project development over quick financial engineering. That is not the posture of a company expecting copper demand to fade.

Rob McEwen, long associated with gold, has been explicit about advancing and monetizing copper assets, arguing that future supply shortages make high quality copper exposure too important to ignore. That kind of capital allocation only makes sense if you believe the price environment has durability.

Then there is Robert Friedland, who has spent years warning that electrification, geopolitics, and underinvestment are colliding into a structural copper shortage. His view has been consistent and simple. The world is still underestimating how hard it will be to bring meaningful new copper supply online.

Technically, the market still looks like a bull that just caught its breath:

The long‑term chart shows higher highs and higher lows, with copper hugging the upper side of its trend bands rather than mean‑reverting.

Volatility has increased, average true range is higher, daily swings are bigger which is all classic behavior in a trend acceleration phase.

So is copper “too expensive”?

Maybe for people who discovered it at the top print.

For anyone thinking over the next three to five years, the honest answer is: we’re paying a higher starting price for a structurally tighter market.

That’s not comfortable. But it’s how most real super‑cycles start to look once the story leaks beyond the niche crowd.

6. How I’m thinking about copper in the metals stack

Let me be very clear: I’m not pivoting from “gold and silver guy” to “copper influencer.”

Gold and silver still sit at the core of my view that fiat dies slowly, then all at once.

But copper deserves a real seat at the table for a few reasons:

It’s the workhorse metal for the energy and AI transitions everyone claims to believe in.

It has a believable deficit story, backed by hard numbers and mine‑level issues.

It’s already showing you it can make new all‑time highs in the middle of global uncertainty, without needing a financial‑media meme campaign to get there.

Here’s how I think about it inside a portfolio:

Core thesis:

Gold = monetary insurance.

Silver = higher‑beta monetary metal that moves faster.

Copper = industrial spine of the next decade’s build‑out.

Where the opportunity is:

Quality copper producers with real assets, decent balance sheets, and leverage to higher prices.

Select developers with world‑class deposits that can get built in a world that suddenly cares about supply security.

I’m less interested in pure hype names riding the word “copper” than in the projects that super‑majors will need to secure if this deficit deepens.

How I treat the volatility:

I expect violent corrections just like in gold and silver.

I’m more comfortable buying pullbacks toward key support levels than chasing blue‑sky breakouts.

I constantly ask the same question I use for precious metals: “Did the underlying story change, or did the price just move?”

If the big houses are roughly right, the next couple of years could see copper grinding or spiking higher from already elevated levels as deficits bite and new supply fails to appear on time.

That’s not a guarantee. It’s a setup.

Copper won’t be at the center of every Fiat’s Funeral issue.

But if we really are living through a broader commodities decade and not just a gold and silver trade, then ignoring the metal that wires the whole thing together would be a mistake.

Fiat always fails slowly, then all at once.

Gold survives every cycle.

Silver moves faster.

Copper builds the world that replaces the last one.

Sincerely,

Mr. Uppy

Investment Disclaimer

This content is for educational purposes only and does not constitute financial advice. Investing involves risk, including possible loss of principal. Consult a qualified advisor and read our full disclosure before making investment decisions.

Subscribe to Fiat's Funeral for more

Get new stories and insights delivered to your inbox. It's free.

Unsubscribe anytime

Comments (0)

Loading comments...